00 Nonwoven Waterproof Materials Solution

The steady expansion of the global construction and infrastructure industries, coupled with increasingly stringent requirements for structural durability and environmental adaptability, has driven a strategic transformation in the waterproofing sector—moving from traditional asphalt coatings toward high-performance waterproofing membranes. In this evolution, the core role of nonwoven fabrics as reinforcement or functional layers has become increasingly prominent. Nonwoven-reinforced membranes not only dominate roofing, underground engineering, and water conservancy facilities but have also become key variables in industrial innovation due to their superior tensile strength, puncture resistance, and excellent compatibility with polymer-modified bitumen.

Global Market Status and 10-Year Forecast

According to authoritative industry data, the global waterproofing membrane market is on a clear growth trajectory. The market valuation in 2024 is approximately $35.83 billion, expected to reach $45.5 billion by 2030, maintaining a Compound Annual Growth Rate (CAGR) of around 4.06%. However, with accelerated infrastructure investment in emerging markets, some optimistic forecasts suggest the market will exceed $50.52 billion by 2033, with a CAGR climbing to 7.8%.

| Evaluation Metric | Valuation 2024/2025 ($B) | Forecast 2030-2035 ($B) | Forecast CAGR (%) |

| Global Market (Conservative) | 35.83 (2024) | 45.50 (2030) | 4.06% |

| Global Market (Aggressive) | 27.89 (2025) | 50.52 (2033) | 7.80% |

| Global Market (Integrated) | 38.78 (2025) | 51.90 (2030) | 6.00% |

| Synthetic Polymer Membranes | 18.78 (2025) | 30.73 (2034) | 7.40% |

| China Waterproofing Market | 13.80 (2024) | 17.80 (2030) | 4.30% |

| USA Waterproofing Market | 4.85 (2025) | 10.40 (2030) | 3.9%–6.4% |

Data Sources: Research and Markets, Grand View Research, Industry Aggregated, Segment Analysis, Regional Data

In terms of installation volume, the global total exceeded 2.4 billion square meters in 2023. Sheet-based membranes account for approximately 54% of the total, while liquid-applied coatings account for 46%. Within sheet-based systems, the utilization of nonwoven reinforcement is extremely high, particularly in modified bitumen and polymer sheet sectors.

Regional Market Analysis

Asia-Pacific: The Global Growth Engine

The APAC region currently contributes between 32.9% and 45.9% of global market revenue.

China: Home to the world’s largest waterproofing industrial cluster. The government-led “Sponge City” initiative is a massive engine, aiming for 80% of urban areas to have rainwater absorption and reuse capabilities by 2030. Despite a slowdown in real estate, infrastructure upgrades and old community renovations are becoming new consumption pillars.

India: Expected to expand at a rate exceeding 7.6% over the next five years. Large-scale metro network construction and industrial park expansions are driving a shift from labor-intensive coatings to factory-prefabricated nonwoven reinforced membranes.

Southeast Asia: Vietnam, Thailand, and Indonesia are heavily influenced by monsoon climates, requiring high standards for moisture and mold resistance. Premium membranes are rapidly penetrating local infrastructure and high-end residential projects.

North America & Europe: Optimization and Regulation

Growth in developed markets has shifted from scale expansion to regulation-driven “Net Zero” transitions.

North America: The Infrastructure Investment and Jobs Act has institutionalized waterproofing requirements for roads and bridges. Demand for low-VOC emissions and energy efficiency has led to the popularity of self-adhered and cold-applied membranes due to their smoke-free, low-energy installation.

Europe: The EU maintains strict requirements for the Life Cycle Assessment (LCA) of building materials. This has boosted the use of recycled polyester fibers (rPET) in nonwoven bases. European leaders like Soprema and Renolit lead in the circular economy, with products certified by rigorous EPD (Environmental Product Declaration) standards.

Middle East: Testbed for Super-Projects and Extremes

Market Dynamics: The Middle East waterproofing chemicals market is valued at $419.1 million in 2024 and is projected to reach $652.4 million by 2033 (CAGR 5.2%). Saudi Arabia holds a 35.45% market share, driven by giga-projects like NEOM and “The Line”.

Demand Characteristics: Extreme heat (exceeding 40°C) and intense UV radiation demand high thermal aging resistance and dimensional stability. APP-modified bitumen membranes dominate due to their high softening points, though demand for Cool Roofs and self-adhesive membranes is surging.

Industrial Moves: International giants are strengthening dominance through local acquisitions, such as Sika acquiring Saudi GulfSeal and Mapei acquiring Bitumat.

Africa: Filling the Infrastructure Gap

Egypt: As the core North African market, the construction of the “New Administrative Capital” and the Suez Canal Economic Zone has generated massive waterproofing demand. A nearly $1 billion desalination project set for 2026 will further drive specialized membrane applications.

Nigeria: Facing a $14.2 billion annual urban infrastructure funding gap, 15 Nigerian states have collectively allocated 10.7 trillion Naira for capital expenditure in FY2026, focusing on roads, schools, and public facilities.

Challenges: Despite potential, high thresholds for localized production remain due to volatile raw material costs and energy deficits (Sub-Saharan electricity access is only approx. 53.3%).

South America: The Potential Speed Leader

South America is predicted to be the fastest-growing region for waterproofing solutions, driven by mining and urban residential renewal.

Market Size: Brazil is the regional engine, with revenues expected to reach $3.818 billion by 2030 (CAGR 6.7%). The broader Latin American market is projected at $4.24 billion by 2034.

Mining Drivers: Chile and Peru require extreme waterproofing for Heap Leach Pads. Reinforced Bituminous Geomembranes (BGM) with thicknesses of 4mm to 5.6mm and composite nonwoven geotextile HDPE membranes are widely used.

Chinese Strategic Layout: Oriental Yuhong is actively using the region as a strategic hedge against domestic real estate fluctuations, notably through the acquisition of Chilean retailer Construmart (approx. $123 million) and the Brazilian company Novakem.

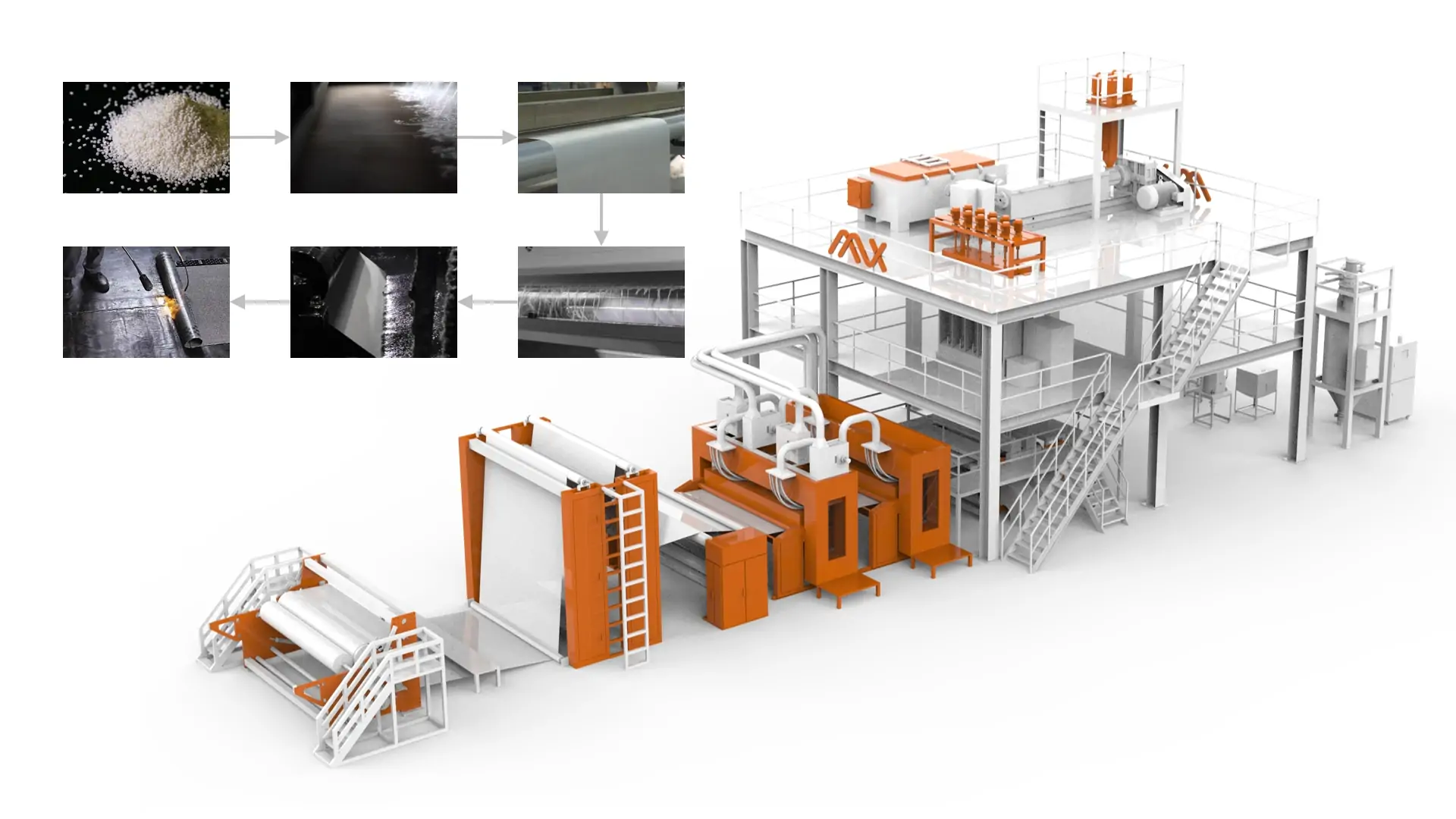

AZX Nonwoven Machinery, a globally renowned and reliable nonwoven machine supplier from China, provides a variety of production solutions for nonwoven waterproof materials based on extensive customer service experience. For nonwoven manufacturers, we analyze these solutions through two major systems based on raw material form (Chips vs. Staple Fiber) and processing depth (Base Fabric vs. Finished Membrane).

1、Polyester Spunbond (Continuous Filament) System

This production route uses polyester chips as the raw material and is characterized by high-strength output and continuous manufacturing.

A. Spunbond Geotextile

Process: Polyester chips are extruded and spun into filaments, which are then formed into a web and reinforced via needle-punching.

Performance: High tensile strength and excellent permeability for filtration and drainage.

Applications: Civil engineering projects requiring soil stabilization and reinforcement.

B. Spunbond Mat for Bitumen Membranes

Process: This follows the spunbond needle-punched line but adds an Impregnation Treatment.

Performance: Enhanced dimensional stability and superior bonding with bitumen.

Applications: High-end base fabric (carrier) for premium bitumen waterproofing membranes.

C. Fiberglass Reinforced Spunbond Mat

Process: Incorporates glass fiber reinforcement during the spunbond and needle-punching phase, followed by impregnation.

Performance: Maximum resistance to thermal expansion and contraction.

Applications: Heavy-duty waterproofing membranes for demanding structural environments.

2、Polyester Staple Fiber (Short Fiber) System

This system utilizes pre-cut polyester staple fibers and relies on mechanical carding to form the web.

A. Staple Fiber Geotextile

Process: Polyester staple fibers undergo Carding followed by Needle-punching.

Performance: Excellent flexibility and high loft, ideal for protective cushioning.

Applications: Filtration, separation, and protection in road and railway construction.

B. Staple Fiber Mat for Bitumen Membranes

Process: The staple fiber web is subjected to impregnation treatment to create a “Polyester Mat”.

Performance: Cost-effective carrier with good bitumen absorption.

Applications: Standard-grade bitumen waterproofing membranes.

C. Fiberglass Reinforced Staple Mat

Process: Adds a fiberglass reinforcement layer to the staple fiber carding and needle-punching line.

Performance: Improves the tensile strength of the staple fiber base to meet higher engineering standards.

Applications: Reinforced carriers for specialized waterproofing tasks.

3、Final Product: Bitumen Waterproofing Membrane

Regardless of whether a Spunbond or Staple Fiber base is used, the final conversion into a finished membrane follows these steps:

Reinforcement Base: Selection of the polyester mat (Spunbond or Staple, with or without Fiberglass).

Bitumen Coating: The mat is passed through a bitumen coating process.

Finished Product: The result is a Finished Waterproofing Membrane ready for site application (e.g., torch-on roofing).

Technical Comparison Table

| Feature | Spunbond System | Staple Fiber System |

| Raw Material | Polyester Chips | Polyester Staple Fibers |

| Web Formation | Direct Spinning | Carding |

| Filament Type | Continuous | Short/Discontinuous |

| Strength | Very High | High |

| Best Use | High-performance infrastructure | Standard construction & civil works |

4、Technical FAQ for Nonwoven Manufacturers

The distinction lies primarily in the processing depth and the intended application:

Geotextile: This is the “raw” fabric produced directly from the needle-punching line. It is used for filtration, drainage, and soil separation in civil engineering.

Polyester Mat (Base Fabric): This is a geotextile that has undergone Impregnation Treatment. This chemical treatment stiffens the fabric and prepares it to be coated with bitumen.

Reinforced Mat: This material includes an extra layer of Glass Fiber (Fiberglass) during the production process. This reinforcement significantly limits thermal shrinkage and increases the tensile strength of the final waterproofing membrane.

The choice depends on your target market’s quality requirements and your budget:

Material Input: Spunbond lines use Polyester Chips , while Staple lines use Polyester Staple Fibers.

Performance: Spunbond (Long Filament) provides superior mechanical strength and puncture resistance because the fibers are continuous. Staple Fiber (Short Fiber) is more flexible and offers better “bulk” or loft.

Selection Logic:

Choose Spunbond for high-end, high-specification infrastructure projects and premium waterproofing brands.

Choose Staple Fiber for general construction, standard-grade waterproofing, or projects where cost-efficiency is the priority.

Your choice should be guided by your position in the supply chain:

To sell to construction contractors: Invest in a PET Spunbond or Staple Needle-punched Geotextile line to produce finished rolls for soil work.

To sell to waterproofing factories: You need the Impregnation Treatment modules to produce the “Mat” (Base fabric) used as a carrier.

To produce the final retail product: You must add a Bitumen Coating line to turn the polyester mat into a Finished Waterproofing Membrane.

Although this article outlines the standard processes for various technologies, AZX Machinery offers customized production line services.

Geotextile Lines: Typically range from 3.2 meters to 6 meters to cover large areas in civil engineering.

Waterproofing Mat Lines: Usually standardized between 1 meter and 2 meters to match the common width of commercial bitumen rolls.

Yes. The production flow shows that Fiberglass Reinforcement and Impregnation Treatment are modular steps. AZX Machinery designs these lines so that a basic needle-punching unit can be integrated with reinforcement modules to produce higher-value materials as your business grows.

Contact Us

As a professional nonwoven machinery manufacturer, AZX has compiled standard surgical gown material (ARAS Nonwoven…

At this exhibition, AZX Group will highlight our nonwoven production line technologies. Include: SSMMSS, SSMMS,…

AZX Nonwoven Machine will participate in the Nonwoven Expo Bangladesh 2025 (July 24-26, booth 61-Hall-4).…

If you operate a nonwoven machine, you know the frustration of polymer residue accumulating on…

The structure of the suction air box significantly affects the web density and hydrostatic pressure…

Complementary Effect in the Web Forming Process In the SMS spunbond nonwoven production line, the…